I was part of what was known as the “R&D” department at Four Star Stage Lighting. One of our responsibilities, was constructing “specials”. Specials included star drops, lighting effects, electrifying scenery – essentially anything that wasn’t standard stage lighting.

When we received the plans for a special, we would research the components that the designer spec’d or that would achieve the effect they wanted, we would figure out how to circuit and wire it, and then estimate the cost of the parts and how many man-hours it would take to accomplish. We would the total all the figures and give a number to Frank DeVerna, the shop owner, so he could give a price to the producer.

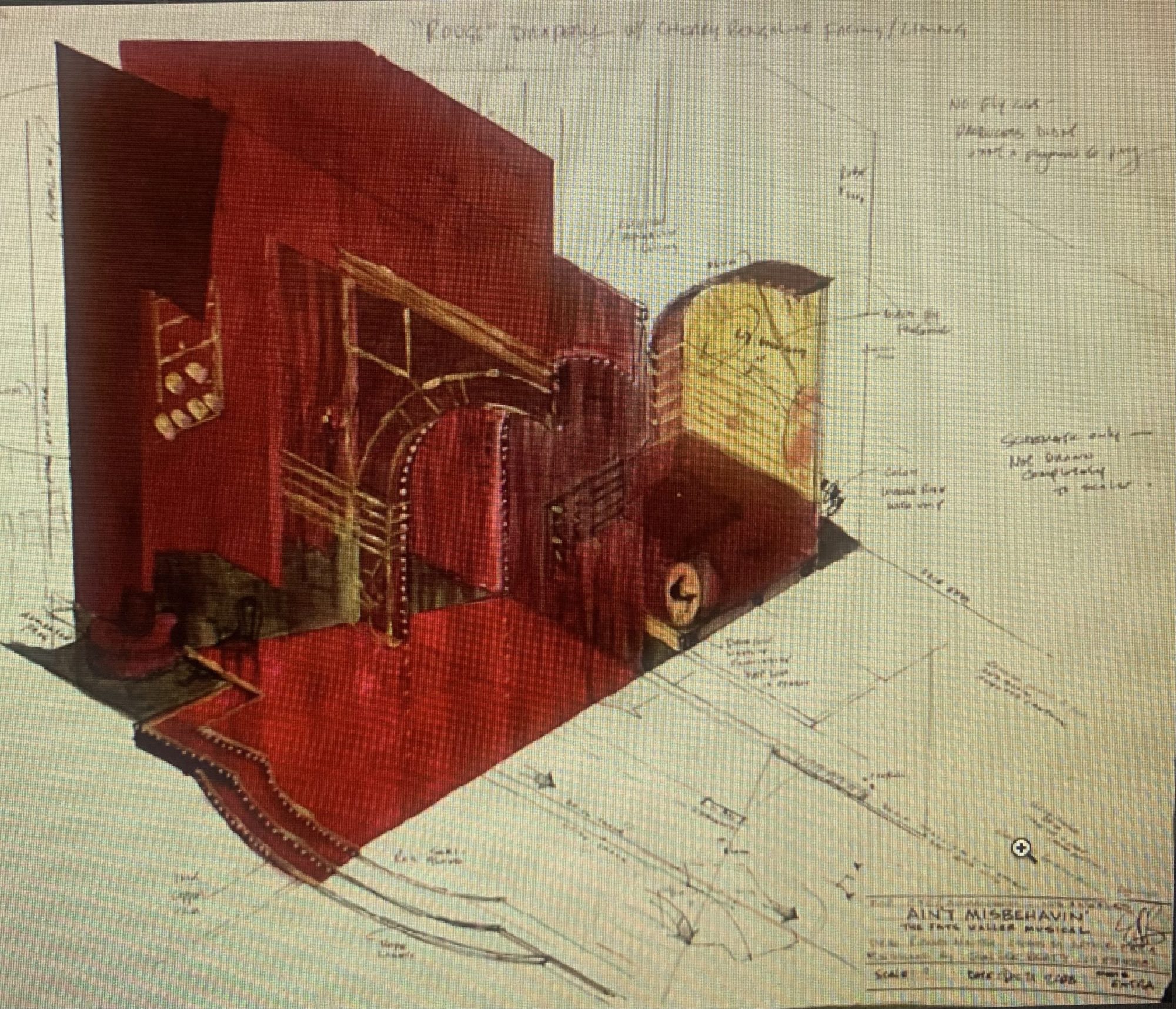

Early in 1978 we were given the plans to “Ain’t Misbehavin’”. The scenery was designed by John Lee Beatty; Pat Collins was the lighting designer. The show had quite a lot of lighted scenery, both back-lit and with exposed chasing lights – so there were lots of different lamps and colors, and it required various mounting and wiring methods. This was our biggest specials project so far and it took us a while to spec all the parts and get prices. We finished our pricing and gave it to Frank. He would let us know if and when it was a ‘go’.

Some days later Myles Ambrose, our department foreman, was called in to the office. The “Ain’t Misbehavin’” people were here and they wanted to see the itemized bid so they could make changes to fit their budget. However, Frank had given them a new total – much different from our original total. All of a sudden our itemized prices and subtotals didn’t add up to the price Frank had given them. We quickly realized we had to run the estimating process backwards – start with the new total and work our way back to new itemized costs! Pat Collins started to follow us into our office. We asked her to give us a few minutes to gather all the papers and organize them. We gathered our notes, parts lists, estimates, lots of legal pads and a calculator – this was before personal computers were common. We took the percentage difference of the bids and applied it to the subtotals of labor and parts, then divided those by the number of hours or number of parts. Now we had new parts costs and hourly labor costs. But we assumed Pat would know the going cost of some of the items, like colored light bulbs and sockets, from browsing the lighting shops on the Bowery and Canal street.

Pat appeared in the office doorway to look at the bid. We gave her another bogus reason we needed more time to get everything together and she left again. We decided to hide in the warehouse part of the building and do our work there. We took all the costs that we thought Pat would be familiar with and reset them close to their true cost and transferred the difference to other parts that she might not know. We also changed part quantities and labor estimates to help offset our changes. We did several iterations of this until we thought we had reasonable numbers that added up to the new total.

Pat finally found our last hiding place. She was persistent and by this time she must have wondered what was going on (or maybe she knew!). We still had to take all our calculations and transfer them to a proper bid document, so we told her we’d be with her in a few more minutes. We finally finished and Myles presented the new bid to Pat.

We learned a lot about the bidding process that day! “Ain’t Misbehavin’” was a success and we eventually outfit four companies – Broadway and three tours.